The commercial real estate crisis is unfolding as office vacancy rates soar and demand for urban workspace dwindles, raising concerns about its long-term impact on the economy. With a significant portion of real estate loans maturing in the coming years, the financial landscape appears shaky, especially for smaller banks previously deemed stable. Analysts warn that rising interest rates, coupled with ongoing bank failures and potential loan defaults, could exacerbate an already precarious situation. As investors grapple with dwindling property values and an influx of delinquent commercial loans, the economic ramifications could ripple throughout the banking sector and beyond. The stakes are high, as many fear that this crisis might escalate into a broader financial downturn, challenging the resilience of the entire market.

The ongoing turmoil in the commercial property market signals a looming financial conundrum that cannot be ignored. Terms such as the commercial property predicament and the office space downturn encapsulate the challenges faced by this sector, particularly amid escalating office vacancy statistics. As financial institutions confront the potential fallout from real estate investment failures, the repercussions could extend to various facets of the economy, influencing lending practices and consumer confidence. The interplay between rising interest levels and the looming threat of a bank crisis creates a precarious environment ripe for instability. The urgency to address these looming issues is paramount for businesses, investors, and policymakers alike.

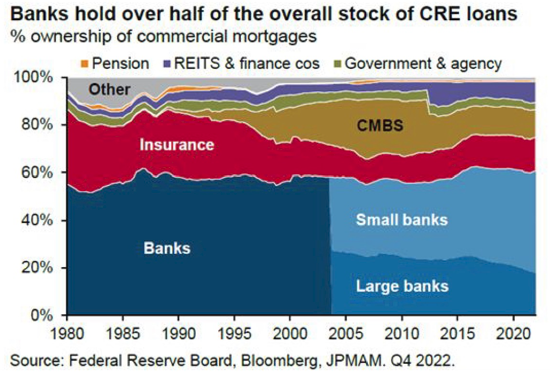

Understanding the Commercial Real Estate Crisis

The commercial real estate crisis is deeply intertwined with high office vacancy rates that have surged since the pandemic. With demand for office space plummeting, cities like Boston are witnessing vacancy rates soaring between 12% to 23%. This drastic decline not only diminishes property values but also raises concerns about potential bank failures, especially as a significant wave of commercial real estate loans comes due by 2025. As banks adjust to these conditions, they may face increased delinquencies that ripple through the financial system, raising alarms over stability and economic impact.

Experts warn that the repercussions of a commercial real estate crisis could be severe, particularly for regional banks heavily invested in these sectors. Approximately 20% of the $4.7 trillion in commercial mortgage debt held by lenders is due this year, emphasizing the urgency of the situation. While larger banks like JPMorgan and Bank of America are relatively insulated due to stringent regulations post-2008 financial crisis, smaller banks may struggle under the weight of defaults, potentially leading to broader financial instability.

Frequently Asked Questions

What is the current status of commercial real estate vacancy rates and their impact on the economy?

High commercial real estate vacancy rates, particularly in office spaces, currently range from 12% to 23% in major U.S. cities. This influx of vacancies is depressing property values and poses risks of significant losses to investors and lenders, potentially impacting the broader economy.

How are bank failures related to the commercial real estate crisis?

Bank failures are increasingly linked to the commercial real estate crisis as many lenders hold substantial amounts of real estate loans. With a significant portion of these loans due by 2025 and high vacancy rates leading to delinquencies, regional banks may face challenges that can trigger failures.

What economic impact do rising interest rates have on commercial real estate loans?

Rising interest rates have resulted in over-leveraging within the commercial real estate sector, making it difficult for property owners to refinance their loans. As a result, many borrowers may default, posing a risk to banks and the overall economic stability.

Are commercial real estate loans leading to a financial crisis similar to 2008?

While the commercial real estate crisis presents serious risks, particularly for smaller banks, experts suggest it won’t replicate the 2008 financial crisis. The current banking regulations and the overall robust job market provide some buffers against widespread financial meltdown.

What sectors are most affected by the commercial real estate crisis?

The office sector has been heavily impacted, particularly due to changes in work habits post-pandemic, leading to high vacancy rates. However, certain segments within commercial real estate, such as premium buildings, still maintain demand.

Can the commercial real estate crisis be mitigated or solved?

The commercial real estate crisis might be somewhat mitigated if interest rates decrease, allowing for easier refinancing. However, with the current economic outlook, significant adjustments, including potential bankruptcies, are likely necessary before recovery.

What effect might a wave of delinquent commercial real estate loans have on regional banks?

A wave of delinquent commercial real estate loans could significantly affect regional banks, leading to tighter lending practices and reduced consumption in local economies, especially since these banks have substantial exposure to this sector.

How prepared are major banks to handle potential commercial real estate losses?

The six largest banks in the U.S. are more diversified and generally better prepared to absorb potential losses from the commercial real estate crisis due to their strong profit generation in other areas and the overall effects of high interest rates.

What long-term trends are expected in commercial real estate following the current crisis?

Long-term trends in commercial real estate may include a shift toward more sustainable and flexible buildings. However, many forecasts suggest that despite current struggles, interest rates may stabilize, correcting some aspects of the market over time.

What are the potential consequences for consumers due to the commercial real estate crisis?

Consumers may face indirect consequences through pension fund losses and potential reductions in regional bank lending due to the commercial real estate crisis, which could decrease disposable income and overall economic activity.

| Key Point | Details |

|---|---|

| High Office Vacancy Rates | Vacancy rates range from 12% to 23% in major U.S. cities, depressing property values. |

| Commercial Mortgage Debt | 20% of the $4.7 trillion in commercial mortgage debt is due this year. |

| Potential Bank Failures | Widespread bank failures are unlikely but some smaller banks may struggle or fail. |

| Investor Optimism | Many investors believe interest rates will eventually drop and that they will recover. |

| Impact on Economy | Potential severe consequences for regional banks, impacting consumption and lending. |

Summary

The commercial real estate crisis could pose significant threats to the US economy, primarily through high vacancy rates and looming mortgage debts. Despite fears of bank failures, experts suggest that the systemic risk remains manageable due to the resilience of larger banks and potential recoveries in the commercial property market. Nevertheless, the interconnectedness of banks and regional economies could lead to cascading economic effects, making it crucial to address these challenges proactively.