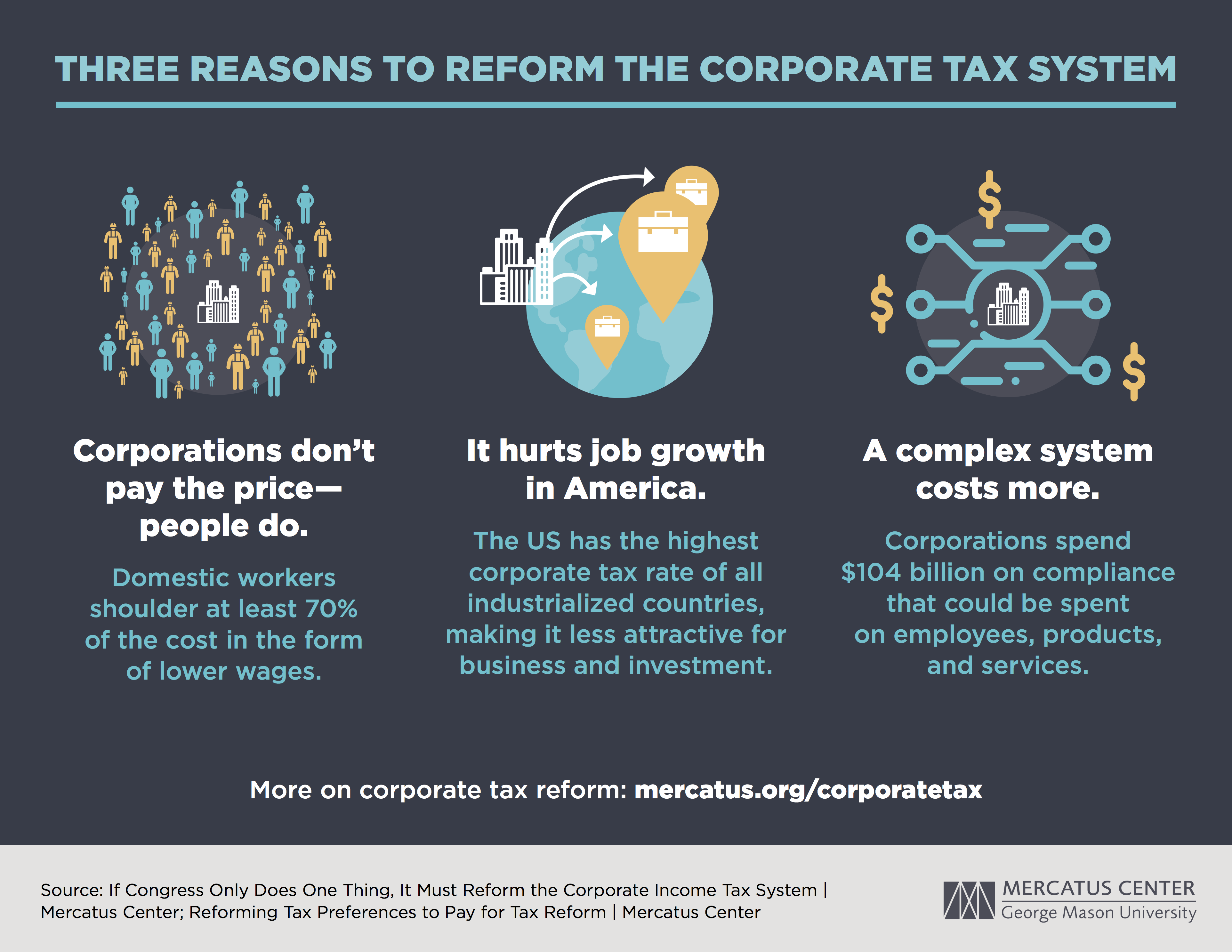

Corporate tax reforms have emerged as a pivotal topic in the ongoing discourse surrounding the U.S. economy, especially in light of the upcoming Congress tax battle. The significant changes brought about by the 2017 Tax Cuts and Jobs Act (TCJA) have been a source of intense debate, with proponents advocating for corporate tax cuts to stimulate growth, while critics argue for raising rates to address increasing budget deficits. Harvard economist Gabriel Chodorow-Reich’s recent analysis sheds light on the economic impacts of tax policy, particularly the ramifications of the TCJA, suggesting that the benefits of tax cuts have been overstated. As parts of the legislation are set to expire, the dialogue intensifies, highlighting the urgent need for effective corporate tax reforms that can balance fiscal responsibility with economic growth. The next steps in this debate could shape the financial landscape for years to come.

Tax code modifications aimed at corporations are increasingly scrutinized as lawmakers prepare for another round of fiscal debates. The 2017 Tax Cuts and Jobs Act (TCJA) featured sweeping changes, specifically designed to adjust corporate tax rates and stimulate economic vitality. Experts like Gabriel Chodorow-Reich are investigating the real-world consequences of such tax strategies, raising questions about whether these corporate tax revisions are fueling growth or simply depleting necessary government revenue. As debates heat up, understanding the nuances between tax reductions and potential hikes becomes imperative for policymakers. The ongoing evaluation of corporate tax legislation will be critical in determining both investment patterns and wage dynamics in the post-pandemic economy.

Analyzing the 2017 Tax Cuts and Jobs Act’s Effect on Corporate Taxation

The 2017 Tax Cuts and Jobs Act (TCJA) marked a significant shift in corporate taxation within the United States, permanently lowering the corporate tax rate from 35% to 21%. This change aimed to stimulate economic growth and increase capital investment by businesses. However, economic analysts, including Gabriel Chodorow-Reich, have scrutinized these outcomes to assess their long-term impacts. His research reveals a modest increase in corporate investments and wages following the tax cuts, but he argues that these gains were insufficient to offset the steep decline in corporate tax revenues.

Chodorow-Reich’s findings suggest that while the TCJA aimed to invigorate economic growth through corporate tax reductions, the expected surge in tax revenues did not materialize as anticipated. The law’s provisions, including the elimination of immediate write-offs for capital investments and research expenses, have faced criticism for failing to benefit low- and middle-income households. As Congress approaches a new tax battle in 2025, the conversation surrounding corporate tax reforms is more pertinent than ever, beckoning a reassessment of the initial promises made by the TCJA.

The Economic Impacts of Tax Policy: Insights from Gabriel Chodorow-Reich

According to Gabriel Chodorow-Reich, understanding the economic impacts of tax policy requires a careful analysis of empirical data over rhetorical assurances from policymakers. His examination of the TCJA highlights that while some corporate entities saw spurts of profit growth, the broad implications of such tax policy designed primarily to catalyze growth cannot merely rely on the allure of tax cuts. Instead, it is crucial to analyze how these changes translate to real wages and investment returns for the wider workforce.

His research indicates that the economic effects of tax policies can be deceivingly simplistic. For instance, many proponents of corporate tax cuts argued that these measures would reflexively lead to more jobs and higher wages, but Chodorow-Reich’s analyses have shown that the correlation may not be as strong as anticipated. In a globalized economy, various factors beyond tax codes can affect corporate behavior. As Congress debates potential reforms, the need for informed discussion grounded in economic evidence is essential to ensure that future tax policies effectively stimulate economic growth without disproportionately affecting public revenue.

Bipartisan Perspectives on Corporate Tax Rates

The discussion surrounding corporate tax rates is deeply partisan, especially as the expiration of certain TCJA provisions looms. In recent debates, Democrats, including Vice President Kamala Harris, call for reinstating higher corporate taxes to fund vital social programs, while Republicans argue that further lowering these rates will promote investment and job creation. This ongoing battle reflects a broader disagreement about the role of taxation in shaping economic strategies. For years, both sides have leveraged the ramifications of the TCJA to bolster their respective positions on fiscal policy.

Amidst this partisan divide, Chodorow-Reich’s findings serve as a critical reminder of the implications of corporate taxation. His work emphasizes that higher corporate taxes do not inherently stifle economic growth; indeed, they may enable governments to invest in public goods that foster innovation and productivity in the long run. The challenge Congress faces is to bridge these differing ideologies to craft a tax structure that equitably addresses revenue needs while nurturing an environment conducive to business growth.

Expiring Provisions: Consequences and Considerations

Key provisions of the TCJA are set to expire by the end of 2025, which raises questions about their expiration consequences for the corporate sector and the wider economy. Many observers are concerned about the potential negative effects of letting these provisions lapse, especially those related to capital investment and research expenses. Chodorow-Reich’s perspective points out that the immediate write-off provisions significantly influenced corporate investment behavior, and losing them may slow the momentum generated by these fiscal incentives over recent years.

The impending expiration offers Congress a unique opportunity to reevaluate the framework of corporate taxation. Instead of merely extending current tax cuts, lawmakers could explore a balanced approach, such as reinstating essential expensing provisions while adjusting statutory rates. This might create a fairer system that promotes sustainable economic growth while generating necessary revenue for public services. As lawmakers prepare for 2025, constructive dialogue on the future of corporate taxes will be crucial for aligning economic objectives with the public’s fiscal interests.

The Evolving Nature of Corporate Taxation

Corporate taxation has undergone significant transformations since the TCJA’s enactment, reflecting broader economic changes and shifting international dynamics. The U.S. corporate tax rate, once average among developed nations, has now placed the country in a more competitive landscape. Analysts like Chodorow-Reich emphasize the need for continuous evaluation and adaptation of tax policies as global economic conditions and domestic corporate behaviors evolve. He argues that a static approach to taxation may undermine the ability of U.S. companies to compete on the international stage.

To effectively navigate this landscape, lawmakers must consider both domestic needs and international realities. The TCJA’s consequences illuminated the careful balance required in tax legislation, showcasing that reductions, while appealing politically, can have complex implications. The focus moving forward should not only be on rates but also on the structures that guide investment criteria, ensuring that corporate taxes stimulate innovation and growth while supporting the economic fabric of the nation.

Corporate Tax Cuts and Their Economic Outcomes

Corporate tax cuts, as introduced by the TCJA, were aimed at spurring economic activity through a reduction in tax burdens for corporations. However, as Chodorow-Reich’s research indicates, the reaction of the economy has not favored such cuts unequivocally. They did lead to an uptick in corporate profits, but the overarching benefit of these tax decreases on employment and wages has not yet materialized to the extent advertised. Reductions were implemented with the promise of greater investment and job creation, prompting an ongoing debate over their efficacy.

The real challenge lies in recognizing that while tax cuts can incentivize some financial decisions, they are not a blanket solution for all economic concerns. Chodorow-Reich’s findings encourage a critical perspective on corporate financial strategies; companies respond to an array of factors, not simply tax incentives. Successful tax reforms must integrate a holistic view, incorporating insights into how such policies impact various stakeholders in the economy.

Understanding the Tax Battle Ahead: Anticipating Congressional Action

As the clock ticks toward the end of 2025, anticipation builds regarding the upcoming congressional tax battle. Policymakers will confront the expiration of the significant provisions of the TCJA and the ongoing debate over corporate tax reforms and revenue generation strategies. Compounding this scenario, the internal dynamics of both parties will further influence legislative actions, as they aim to position themselves favorably before voters in the next election cycle. The insights from economists such as Chodorow-Reich are vital as they frame these discussions in terms of factual evaluations versus political rhetoric.

Additionally, the implications of the TCJA’s corporate tax cuts underscore the importance of thoughtful deliberation. As Congress navigates a bipartisan approach to tax reform, the potential to incorporate evidence-based policy proposals may inspire more productive outcomes. By addressing both the fiscal responsibilities and the economic growth imperatives, lawmakers could develop a tax strategy that addresses the contemporary realities of a globalized economy.

The Future of Taxes: Reforms for Sustainable Growth

The urgency for tax reform remains a key issue as lawmakers consider adjustments to corporate tax rates and the fading provisions of the TCJA. With a more competitive global environment and evolving economic landscapes, the need for a future-ready tax system is unprecedented. Chodorow-Reich’s research points to the sustainable growth opportunities ripe for exploration, suggesting that reform should prioritize incentives that truly fuel economic expansion and benefit the broader society.

Continued dialogues surrounding the expiration of beneficial tax provisions can open avenues for innovative reform. Emphasizing investment in domestic capabilities and workforce development will also contribute to paving a pathway for sustainable economic stability. As such reforms are drafted, it will be instrumental for legislators to bear in mind the complexities that govern corporate investment behaviors and to craft policies that foster long-term growth instead of short-sighted gains.

Rethinking Corporate Tax Policy: Lessons from the TCJA

The analysis by Chodorow-Reich and his colleagues provides crucial lessons about the impact of corporate tax policy initiated under the TCJA. As the expiration deadline approaches, a reexamination of these lessons is critical for informing future legislative efforts. The data suggests that the anticipated economic growth associated with tax cuts often comes with caveats, demonstrating that the relationship between tax legislation and economic outcomes is intricate and nuanced.

Notably, the TCJA was aimed at fostering a business-friendly environment; however, the observed drop in tax revenue and mixed results in corporate investment indicate a need for a strategic rethink. This focus on evidence-based policymaking will help expose the shortcomings of prior tax cuts, potentially preventing similar missteps in future reforms. By recognizing the lessons learned from the TCJA, lawmakers can devise a tax structure that balances corporate welfare with the fiscal health of public coffers.

Frequently Asked Questions

What are the key provisions of the 2017 Tax Cuts and Jobs Act (TCJA) related to corporate tax reforms?

The 2017 Tax Cuts and Jobs Act (TCJA) significantly reformed corporate tax rates by reducing the statutory rate from 35% to 21%. It introduced provisions allowing companies to fully deduct the cost of certain capital investments and research expenses immediately. These changes aimed to stimulate business investment and economic growth, though their effectiveness remains a subject of debate.

How did Gabriel Chodorow-Reich evaluate the economic impacts of tax policy following the 2017 Tax Cuts and Jobs Act?

Gabriel Chodorow-Reich, in his analysis of the TCJA, found that while corporate tax cuts did lead to increased investment by approximately 11%, the overall economic benefit was modest compared to the significant drop in tax revenue, which fell by 40% post-implementation. His research emphasizes that corporations are indeed influenced by tax policy, contradicting views that tax rates have little impact on corporate behavior.

What is the current debate surrounding corporate tax reforms in the context of the 2017 Tax Cuts and Jobs Act?

The ongoing debate in Congress over corporate tax reforms centers on whether to maintain, increase, or further cut corporate tax rates as key provisions of the TCJA are set to expire. Politicians like Kamala Harris are advocating for higher corporate rates to fund various social programs, while proponents like Donald Trump argue that further cuts would boost economic growth. This conflict reflects the broader discourse on the economic impacts of tax policy.

What were the observable effects on corporate tax revenue following the implementation of the TCJA?

Following the enactment of the TCJA, corporate tax revenue initially declined by about 40%. However, starting in 2020, corporate tax revenue began to recover significantly as businesses reported soaring profits. This rebound raised questions about the long-term impacts of tax reforms on revenue and corporate behavior, prompting further analysis of economic conditions during the pandemic.

What is the anticipated outcome of the upcoming Congress tax battle regarding corporate tax rates?

The anticipated outcome of the Congress tax battle regarding corporate tax rates is uncertain. As provisions of the TCJA are set to sunset in 2025, lawmakers are debating whether to reinstate higher corporate taxes or extend existing cuts. This includes discussions on balancing tax rates with effective measures to encourage investment and innovation, as highlighted by recent studies, including those from Gabriel Chodorow-Reich.

| Key Points | Details |

|---|---|

| Tax Battle Ahead | Congress is preparing for discussions on the expiring provisions of the Tax Cuts and Jobs Act (TCJA) in 2025. |

| Debate on Corporate Taxes | The future of corporate tax cuts is debated between raising rates to fund initiatives or further reductions to spur growth. |

| Economic Impact | Research shows modest increases in wages and investment, but significant drops in tax revenue post-TCJA implementation. |

| Need for Reforms | The corporate tax code has seen minimal changes since the 1980s, necessitating a comprehensive reform. |

| Effectiveness of Provisions | Expensing provisions have been more effective at driving investment compared to statutory rate cuts. |

| Corporate Income Tax Revenue | Corporate tax revenues dropped by 40% after TCJA but began to recover with rising business profits. |

| Policy Suggestions | Increased statutory rates combined with reinstated expensing provisions may benefit investments and wages. |

Summary

Corporate tax reforms are at the forefront of upcoming discussions as Congress prepares for a contentious tax battle in 2025. The key lessons from the 2017 Tax Cuts and Jobs Act (TCJA) highlight the complexities and challenges of balancing tax cuts with revenue generation. Research indicates that while tax reductions may spur investment, the substantial revenue shortfall must be addressed thoughtfully. As policymakers navigate these debates, it’s essential to consider evidence-based strategies that not only foster economic growth but also ensure long-term fiscal stability.